According to the Cleveland Clinic, acrophobia, the fear of heights, affects an estimated 3% to 6.4% of the population, making it one of the most common specific phobias [1]. But based on firsthand experience, I’d say nearly 100% of investors have a fear of investing at new market highs. This anxiety is often fueled by the media's frenzy around "stocks at record highs," which can sound like a warning sign. Just as acrophobia can make people afraid to step onto a high balcony, the fear of market highs can make investors hesitate to enter the market at what seems like a precarious moment. However, understanding the dynamics of market highs and employing disciplined investing strategies can help navigate these challenges effectively.

The Human Condition

Biology plays a significant role in how investors perceive market highs. The financial media often creates a frenzy around "stocks at record highs," which can sound like a warning sign. Recency bias makes past market crashes more memorable (2000, 2007, 2022), leading to fears that it’ll happen again in the same manner as before. Losing money after buying feels worse than missing gains because human evolution has led us to be loss averse. It’s how we survived as a species. These two cognitive biases fuel our natural urge to avoid investing when markets are at new highs. So how can we combat it?

Focus on the Data

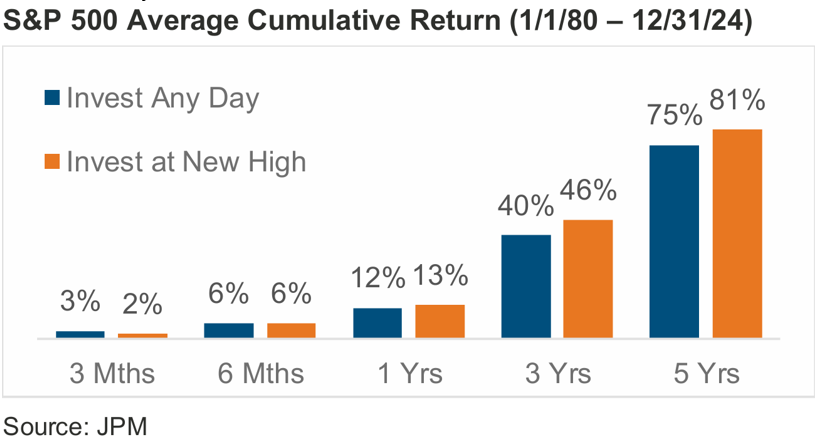

If you strip away the emotion and just look at the data, investing at market highs versus “any random day” has a surprisingly important truth. Historically, investing on days when the market is at a new high can yield similar results to investing on a random day. In fact, over longer investment horizons, investing at all-time highs tends to outperform investing on a random day.

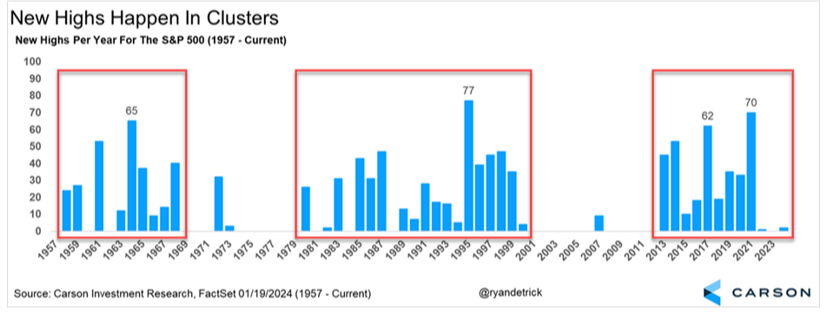

These somewhat surprising results are because market highs tend to cluster together during strong uptrends (see below):

While we never know when a true market peak occurs until after the event, there is psychological churning when buying high and seeing your investment take a quick loss. So, how do you manage investing for those long-term goals with the emotions that go along for the ride?

Dollar Cost Averaging Can Help

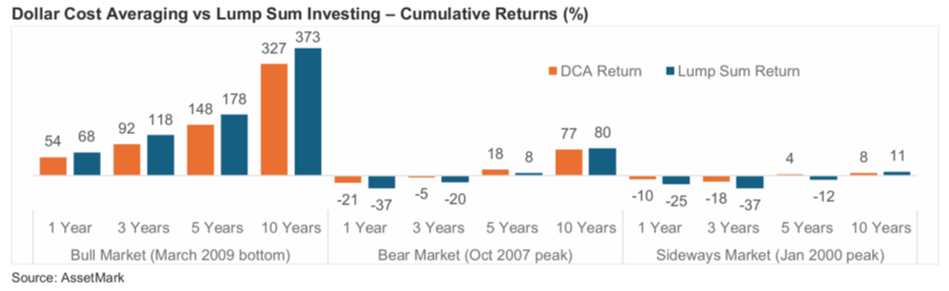

Dollar Cost Averaging (DCA) involves investing fixed amounts of money regularly, regardless of whether the market is high or low. This strategy can cushion some of the losses in the short term and provide a smoother ride during market volatility. For example, using DCA to invest at market peaks, like in 2000 or 2007, saw better returns over the subsequent 5-year period compared to lump sum investing. The DCA portfolios reduced the emotional strain during market volatility. It's like taking small, manageable steps onto the balcony, reducing the fear of falling.

However, over the longer term of 10 years or more, lump sum investors tend to catch up. Lump sum investing can even outperform DCA, but it requires a strong stomach to handle large short-term drops. DCA, on the other hand, is a way to minimize regret, reduce the stress of 'bad timing,' and provide a steadier ride. It's the equivalent of slowly acclimating to the height, making the experience less daunting

Bottom Line

Investing during market highs requires a balanced approach that considers both the emotional and financial aspects. Dollar Cost Averaging can provide a smoother ride during volatile times, while lump sum investing can yield higher returns over the long term. Cutting out emotions and focusing on data are crucial for achieving investment goals. By understanding the dynamics of market highs and employing the right strategies, investors can navigate these challenges effectively and achieve their financial objectives. Just as overcoming acrophobia can lead to enjoying the view from new heights, overcoming the fear of market highs can lead to better investment outcomes and financial success.

Sources:

[1] https://my.clevelandclinic.org/health/diseases/21956-acrophobia-fear-of-heights

Disclosures

This material has been prepared for informational purposes only and should not be construed as a solicitation to effect, or attempt to effect, either transactions in securities or the rendering of personalized investment advice. This material is not intended to provide, and should not be relied on for tax, legal, investment, accounting, or other financial advice. You should consult your own tax, legal, financial, and accounting advisors before engaging in any transaction. Asset allocation and diversification do not guarantee a profit or protect against a loss. All references to potential future developments or outcomes are strictly the views and opinions of Richard W. Paul & Associates and in no way promise, guarantee, or seek to predict with any certainty what may or may not occur in various economies and investment markets. Past performance is not necessarily indicative of future performance.