Robert Shiller is a highly regarded housing expert. His work shows that real estate generally keeps pace with inflation but seldom offers any excess return1. Profits look even less appealing after accounting for repairs, maintenance, transaction fees, property taxes, insurance, and other hidden costs. Returns have been so shockingly poor because of the differences between assets and investments.

An asset is a store of value, while an investment has the potential to generate value over time. Precious metals, art, collectibles, fancy wines, and cars are all examples of a store of value. An asset’s value changes over time solely from the demand to own it and the supply available.

Art hanging on a wall does exactly what silver coins do in a safe or bitcoin does in a digital wallet—nothing. If demand rises for any of these while supply remains fixed, the owner may be able to sell it for a profit.

An investment is more than a store of value because it produces income or measurable growth. Bonds and stocks are investments because the former pay income, and the latter generate earnings that can be reinvested for future growth or paid out in dividends or share buybacks.

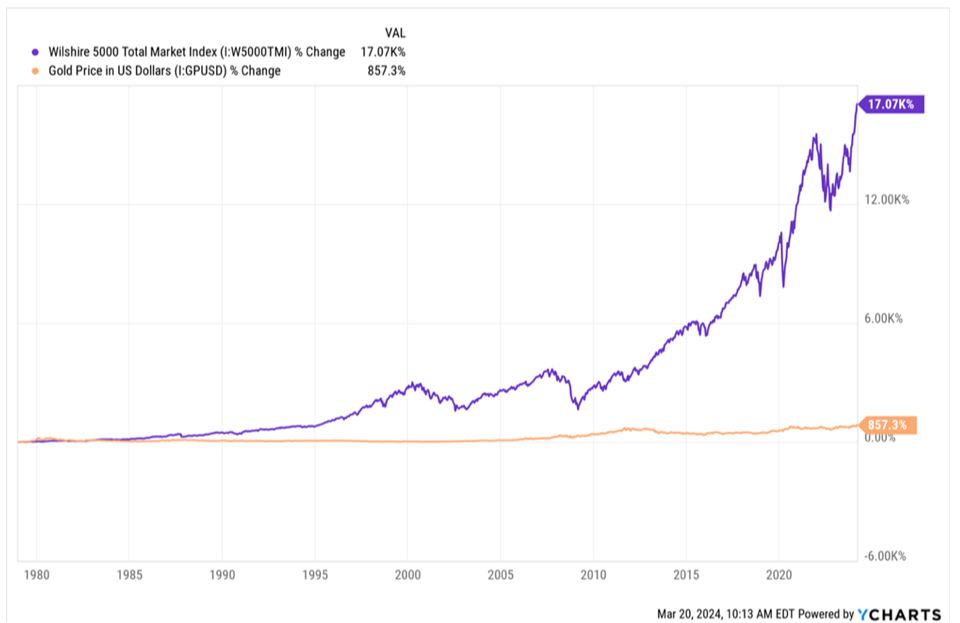

The chart below shows why some assets should never be classified as investments. It compares the performance of the Wilshire 5000 Total Market Full Cap Index (purple line), an equity index comprised of the most publicly traded stocks in the U.S., to the spot price for gold (gold line).

All it takes is a quick glance to accuse gold of being a terrible investment when compared to the broader stock market. However, it’s an unfair comparison because this shiny pet rock suffers from the same limitations as a home.

Gold generates no income, requires expensive storage and insurance costs, cannot compound over time, etc. Since gold does not possess the characteristics of a real investment, it should not be expected to perform like one.

Similarly, homes do not create and sell innovative products or buy rivals to grow market share. They also rarely generate income, and when they do, the cash received from renting that spare bedroom seldom pays the mortgage. Hence, it is equally inappropriate to classify homes with stocks, bonds, and other investments.

Only a select few real estate examples possess the required attributes. Landlords who generate monthly rental income above their costs and restoration experts who repair properties and sell them for a profit can certainly claim to own investments. The rest are just assets.

The bottom line

There is an old saying that where there’s thunder, there’s lightning, but the opposite is not always the case. Just because lightning rips across the sky does not guarantee thunder is right behind. Similarly, investments are assets, but not all assets are investments. Investors can get into trouble when they are unable to distinguish between the two.

Years ago, my wife and I purchased our first apartment in New York City after years of renting. We’re both data junkies, so based on Shiller’s work, renting would have likely been the wiser financial option.

But that wasn’t our goal. We wanted to pick our paint colors, customize a kitchen to suit our needs, and take a few years off from moving (few tortures in this known universe are more painful than moving between apartments in New York City). Homes and other assets often carry “intangible” value that cannot be seen, touched, or quantified.

There’s no question that our decision to buy had an economic component. We certainly hoped to earn a profit, and home ownership does offer financial advantages. For example, we wrote off the mortgage interest and avoided annual rent hikes in a city where prices rise every fifteen minutes.

We also bought in a neighborhood that has historically maintained its value. Leverage works both ways, so we did not want to put ourselves in a situation that would pose an outsized risk to our down payment.

However, at no time did we view this apartment to be part of our investment portfolio because it was not being used to save for retirement, nor was it intended to fund our kids’ college funds. It was a place to live and personalize, but nothing more.

The bottom line is that most financial plans incorporate assets alongside investments. Just don’t rely too heavily on assets to do the job of investments because they can’t.

Sources

1 Robert Shiller, Irrational Exuberance: https://www.amazon.com/Irrational-Exuberance-Revised-Expanded-Third/dp/0691173125/

Disclosures

This material has been prepared for informational purposes only and should not be construed as a solicitation to effect, or attempt to effect, either transactions in securities or the rendering of personalized investment advice. This material is not intended to provide, and should not be relied on for tax, legal, investment, accounting, or other financial advice. You should consult your own tax, legal, financial, and accounting advisors before engaging in any transaction. Asset allocation and diversification do not guarantee a profit or protect against a loss. All references to potential future developments or outcomes are strictly the views and opinions of Richard W. Paul & Associates and in no way promise, guarantee, or seek to predict with any certainty what may or may not occur in various economies and investment markets. Past performance is not necessarily indicative of future performance.