There appear to be more financial and investing myths than there are truths. Dispelling all of them could take a lifetime, so let’s just focus on a few common ones that can get knocked out quickly.

Never invest in all-time highs. There have been 329 all-time highs in the S&P 500 since March 2013, which has pushed the index’s total return up 247%1. All-time highs are meaningless because all-time highs happen all the time. Think of all the generational wealth that has been missed by so many onlookers simply because they watched the market hit an all-time high and decided to wait for a pullback.

Your stock allocation should be 100 minus your age. This assumes every investor has the same risk tolerance, goals, net worth, expense structure, current and expected income, tax bracket, estate makeup, insurance needs, and a hundred other variables that make the financial planning process so critical to achieving long-term goals.

You can’t put a price on education. Advanced degrees are no different than any other investment, so estimating the potential return over time and comparing it to the committed time and capital most certainly can derive a fair market price. Today, most degrees appear to be egregiously overpriced2,3.

The stock market is rigged. The notion that a market this big and closely watched is somehow controlled by a small group of nefarious profiteers could not be further from the truth. The real and only reason why the pros keep winning is because they are just better. Their tools are more sophisticated, and they have PhDs from some of the most prestigious universities in the world. When they lose money, they spend countless hours trying to up their game, and when they win, they aren’t dipping chicken tenders in champagne glasses on YouTube.

Rising national debt is bad for stocks. The chart below suggests that the last half century says otherwise.

The first rule of debt analysis is that the size of the debt, on its own, is completely and utterly meaningless. The real question is if you can afford the debt, and the U.S. has never had an issue paying its bills.

Gold is safer than the stock market. Gold’s average annual return since 1969 is 7.9%, while the S&P 500 returned just over 11%1. Gold’s annualized volatility is 19.2% over the same period, while the S&P 500 is 15.2%. Said another way, the S&P 500 has averaged a 40% higher annual return than gold, and it’s done so with 26% less volatility. That’s because gold produces no revenue, profits, or cash flow. Nor does it reinvest back into itself or pay dividends. It just sits there, and its price is solely determined by the demand to own it.

Fallen stocks bounce back eventually. The Russell 3000 Index measures the performance of the largest 3,000 U.S. companies representing approximately 98% of the investable U.S. equity market. Between 1980 – 2014, roughly 40% of all stocks in the index suffered a permanent 70%+ decline from their peak value4. The numbers were much higher for technology, biotech, and metals & mining. Stocks are often cheap for a reason, so it takes a lot more than just valuation to value a stock.

Bonds always lose money when interest rates rise. Yes, when rates rise the price of a bond falls, but that fails to account for the income portion of the total return of a bond. From 1954 - 2017, roughly 46% of the months that experienced rising rates still netted a positive return for five-year Treasury bonds2. Meaning, it’s not as simple as assuming bonds are doomed if/when rates start rising again.

China owns most of our debt and by extension owns us. I have no idea where this one started, but China only owns about 4% of U.S. government debt5. Total foreign ownership is at 25%5, meaning 75% is owned by the U.S. government and domestic investors. But even if China owned 80% of our debt, it’s not collateralized like a mortgage, so there’s nothing they could do if we defaulted.

Financial news is news. Investing is boring. It just is. Economies and markets change over time, but nowhere near the speed at which they are being reported these days. There’s also no logical explanation for having this many networks dedicated to reporting financial news 24/7. If the airwaves are not packed with real news, that means stories are filling the gaps.

Stop losses cap the downside. Despite the name, stop losses don’t guarantee execution at a specified price. Once a stop loss is triggered, the order is entered as a “market order,” which executes immediately at the best available price. During periods of extreme volatility, this price could be way lower than expected.

Cash is king. Some cash is king, but there are different types of cash. There’s the critical cash that pays bills and stands ready to pay for emergencies and unexpected circumstances. This should never be put at risk, but there’s also excess cash. This is the cash that doesn’t need to be there. Maybe it’s there due to laziness or perhaps fear of what could happen next. This cash is losing money safely and is by no means king.

Gold will keep you safe through the zombie apocalypse. The world does not end all that often, and even if it were to, what will gold do? Currently, over 90% of demand for gold comes from India and China6. That tells me the rest of the world might not see gold the same way. Add to this the risk of dodging zombies all day, and I can’t see how gold provides any value at all. It’s hard to transport due to its weight, nor can it be divided up easily to pay for goods without proper tools. And unless gold is kept under the mattress, you’re going to need to go get it before the apocalypse sets in. Good luck getting it out of the bank or wherever it’s being stored.

Renting is lighting money on fire. Oh yeah? Try owning a house. Add up all the maintenance costs, friction costs to transact, insurance, weather damage, “Acts of God” that are uninsurable, and taxes that adjust at the whim of local governments. Then layer on the risk of locking yourself into a single locale, levering up to psychotically high levels for that mortgage, and your neighbor selling at 20% below market because they need cash. All this for an “investment” that has failed to beat inflation over the long run. There is nothing at all wrong with renting.

Low trading activity implies my money manager is asleep at the wheel. The legendary investor Jim Rogers famously said that most successful investors do nothing most of the time. I’d even go as far as to say the amount of trading has absolutely no bearing of how hard a money manager is working. Some of the best investors may make a handful of trades each year, while some of the worst may trade all the time because they might actually believe this myth.

Don’t start saving for retirement until you are in your 40s. Let’s say you want to retire at 65. If you invest $10,000 into an S&P 500 index fund at 45, contribute $100 each month, and then assume the long-term average annual return on the index of 10%1, then in 20 years you will have $136,000. If you start at 35, giving yourself an extra 10 years, you’ll have almost $372,000. That’s almost tripling your money by increasing your holding period by 50%. If you start at 25, you’ll have almost $984,000, or over 7 times as much for twice the holding period. This is the power of compounding, so get your kids and grandkids in this game as soon as possible.

China’s renminbi will replace the U.S. dollar as the world’s reserve currency. As of 2019, more than 88% of foreign exchange trading involved the dollar7, and nearly all commodities are priced in dollars. It also dominates as a payment currency for global trade with a 79.5% share of currency usage in value8. The USD also represents 59% of all known central bank foreign exchange reserves9. The next closest is the euro at 21%, so there is nowhere near enough euro in circulation, let alone any other currency, to replace the total value of dollars held. Comparatively, China’s renminbi accounts for around 5% of international trade7 and 2.1% of central bank reserves10. Given China’s blatant manipulation and strict currency controls, it’s hard to envision how they could unseat the dollar.

The S&P 500 is a good benchmark for financial goals. The S&P 500 represents a committee picking stocks for a product that generates hundreds of millions in licensing fees. Does this sound like something you want to benchmark your financial future against? Personally, I’ve never met an investor whose liabilities were tied to the S&P 500, and I can’t imagine I ever will.

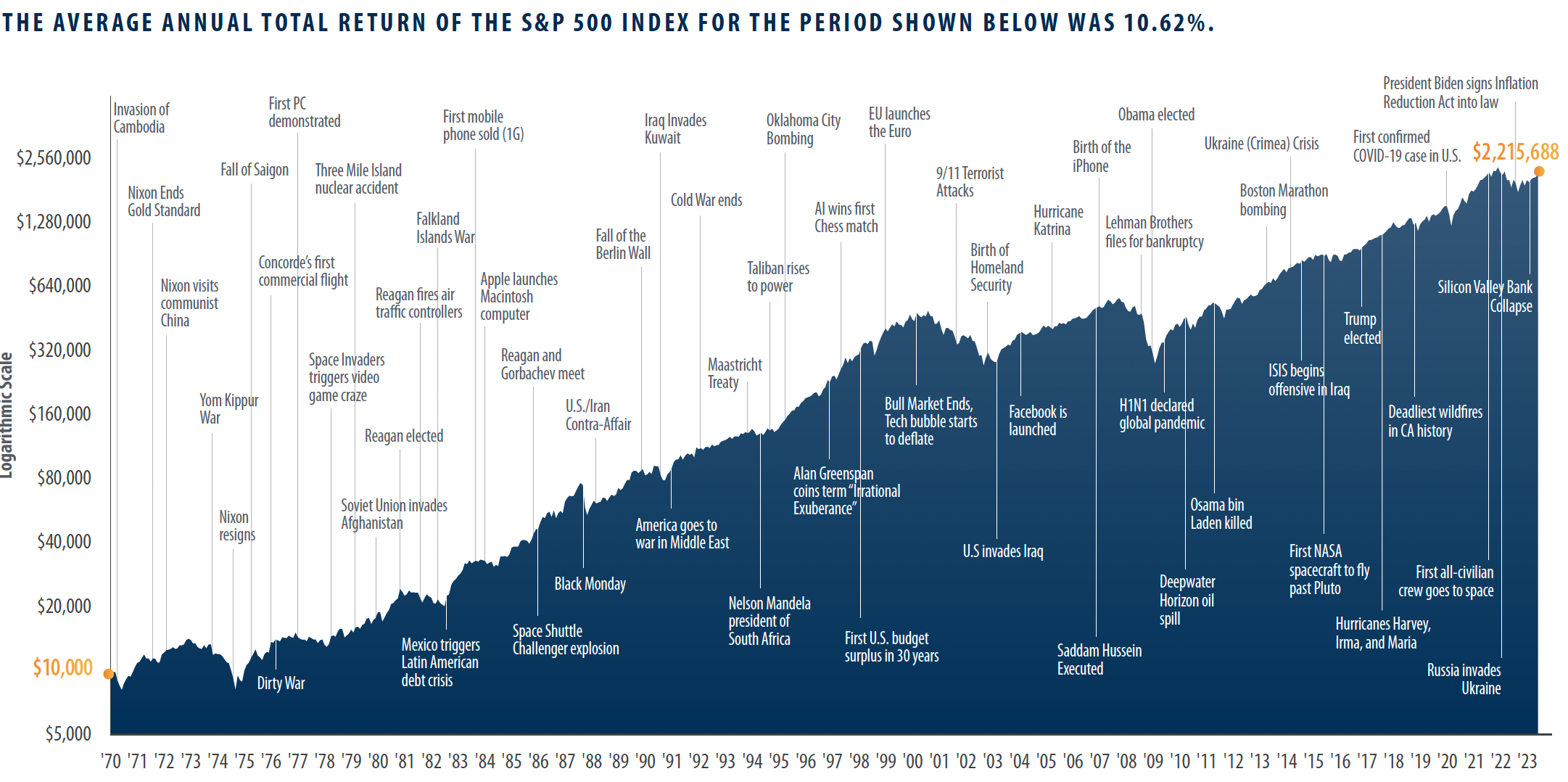

Volatility is a measure of risk. Volatility is a measure of the short-term movements in stock prices. Since the daily ups and downs are driven by emotional reactions to events like the ones in the chart below, then by association, volatility is a measure of emotion. Hence, when the stock market gets more volatile, it’s really just getting more emotional. Sentiment can’t derail a $22 trillion economy on its own, so most market temper tantrums aren’t a sign of any real risk to long-term investors.

Annual returns matter a lot. A year is nothing more than the time it takes for the earth to circle a huge ball of gas. Markets do not operate on calendars, where somehow on January 1st of every year the drivers of the stock market change. Instead, markets are event driven. Meaning, things have to happen for markets to move, and these “things” have nothing to do with calendars 98% of the time. Perhaps this is why Warren Buffett has underperformed the S&P 500 one out of every three years since 1965, yet he’s outperformed the index in aggregate by 2.8 million percent11.

Sources

1 Bloomberg, as of 9/16/2021

3 https://theundercurrent.org/the-credibility-cartel-how-accreditation-leaves-students-in-the-dark/

4 The Agony & The Ecstasy – The Risks and Rewards of A Concentrated Stock Position, J.P. Morgan 2014

5 U.S. Treasury, as of 2021

6 World Gold Council – 2020

7 https://www.bis.org/statistics/rpfx19.htm

8 https://www.swift.com/sites/default/files/documents/swift_bi_currency_evolution_infopaper_57128.pdf

9 https://en.wikipedia.org/wiki/Reserve_currency

11 https://www.berkshirehathaway.com/2020ar/2020ar.pdf

Disclosures

This material has been prepared for informational purposes only and should not be construed as a solicitation to effect, or attempt to effect, either transactions in securities or the rendering of personalized investment advice. This material is not intended to provide, and should not be relied on for tax, legal, investment, accounting, or other financial advice. You should consult your own tax, legal, financial, and accounting advisors before engaging in any transaction. Asset allocation and diversification do not guarantee a profit or protect against a loss. All references to potential future developments or outcomes are strictly the views and opinions of Richard W. Paul & Associates and in no way promise, guarantee, or seek to predict with any certainty what may or may not occur in various economies and investment markets. Past performance is not necessarily indicative of future performance