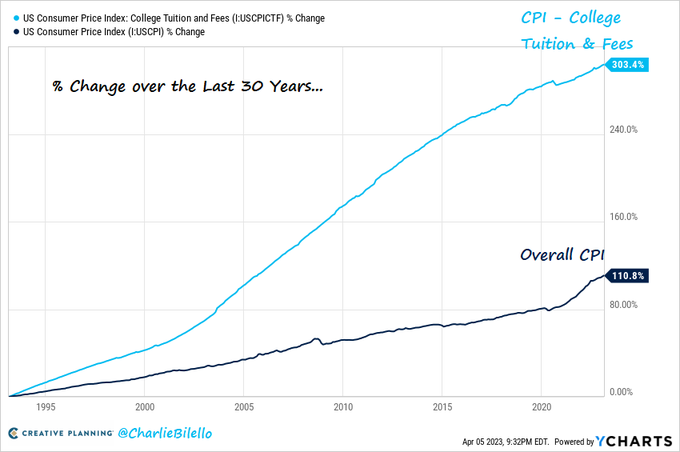

The expenses associated with higher education continue to climb. As seen on the graph below, in the last three decades, education costs have increased at approximately 3x the rate of the overall CPI.

Out of curiosity, I looked at the price per credit hour of my alma mater, Michigan State University, in the year I was born: In 1988, one credit hour cost $56 and in 2023 this number had ballooned to $522 per credit, nearly a 10x increase over my lifetime!

Given this significant increase and the recent restart of student loan payments, it's understandable that families are now paying careful attention to their 529 plans.

Though college costs have skyrocketed, some owners of 529 plans have found themselves with remaining balances, which can present challenges when deciding how to manage these unused funds. This article aims to offer some guidance in navigating this situation.

Background on the 529 plan

While most are familiar with the basic premise of a 529 plan, its primary allure is its tax-advantage benefit, as funds deposited may be state tax deductible, the funds grow tax-free, and you can withdraw them tax-free so long as they’re for qualified educational expenses.

There could be various reasons for having leftover funds, including situations such as:

- Receiving scholarships

- Going to a more affordable college

- Opting out of college

- Overestimating the expenses associated with college

- Inheriting/Receiving gifted funds from relatives

- Graduating ahead of the anticipated schedule

Although the funds in a 529 plan do not have an expiration date, account owners will face a 10% penalty if they utilize them for non-educational purposes. It's important to note that this penalty applies solely to the earnings portion and not to the original contributions.

Having excess funds in a 529 plan presents both challenges and opportunities, underscoring the importance of understanding available options. While these plans are primarily designed for educational expenses, life's unpredictability can occasionally lead families to accumulate more funds than expected.

Here are four strategies to avoid the withdrawal penalty.

- Use 529 funds for additional education or training

We all know the journey of education and personal development is ongoing. Many college graduates are seeking education post college, whether that be a postgraduate master's program or professional certification. For instance, in my field, funds in a 529 plan could have been used for the education/cost of the CFP® program. Investing in these specialized certifications or vocational training can provide practical skills that dramatically improve career prospects.

- Transfer the 529 balance to another beneficiary

As family situations and educational needs change, transferring a 529 account to a different beneficiary can be wise. After one child completes their education, you can move the remaining funds to their sibling or another family member. If you don’t have other family members to transfer to, you can also leave the funds in the plan and apply it to future grandchildren many years down the line.

- Pay student loans with 529 funds

Under the SECURE Act of 2019, you can allocate up to $10,000 from a 529 plan towards repaying federal or private student loans. For example, if a client's son has an $18,000 student loan balance, using $10,000 from his remaining 529 funds can reduce the balance to $8,000, easing the payment burden. However, it's essential to remember that this penalty-free option applies solely to student loans, not other debts like credit cards or mortgages. Additionally, some states may consider using 529 funds for loan repayments as non-qualified, potentially subjecting them to state income tax.

- Roll extra 529 dollars into a Roth IRA

The SECURE 2.0 Act has introduced a new option for leftover 529 funds: transferring balances to a Roth IRA. Beginning in 2024, 529 plan owners can convert up to $35,000 tax-free and without penalties. This move represents a strategic shift towards retirement planning. A $35,000 investment, if compounded at 10% for 35 years, grows to nearly $1 million, all tax-free!

However, there are limitations on this; for instance, your 529 account must have been open for over 15 years, the funds you wish to roll over must have been in your 529 for at least five years, and the rollovers are subject to annual contribution limits. Here is an article from Fidelity explaining this option in more detail: https://www.fidelity.com/learning-center/personal-finance/529-rollover-to-roth

529 transfers, distributions, and rollovers

Regardless of your choice regarding the remaining balance in a 529 account, you have three potential options: a 529 rollover, a 529 transfer, or a 529 distribution. Here's a brief overview of each:

- 529 rollover: This involves moving your 529 savings into a Roth IRA, typically starting with a withdrawal request form. While technically considered a distribution, it's commonly referred to as a rollover. This option becomes available in 2024, subject to state-specific guidelines.

- 529 transfer: A straightforward solution is to change the beneficiary of your existing 529 account. As the account owner, you can initiate this process through the 529 plan's website. However, be mindful that transferring the plan to a non-qualified individual may result in penalties and taxes.

- 529 distribution: Withdrawing funds from a 529 account is a simple process, often done through an online account or by completing a withdrawal request form. It's important to note that funds used for qualified educational expenses or student loan repayment (up to $10,000) are penalty-free. However, using them for other purposes may incur taxes and penalties.

Next steps for your 529 plan funds

Managing leftover funds in your 529 account can be tricky. While doing it yourself might seem easy, 529 rules can be nuanced. Consulting with your financial planner can help you understand options and decide what aligns with your family’s financial goals.

Disclosures

This material has been prepared for informational purposes only and should not be construed as a solicitation to effect, or attempt to effect, either transactions in securities or the rendering of personalized investment advice. This material is not intended to provide, and should not be relied on for tax, legal, investment, accounting, or other financial advice. You should consult your own tax, legal, financial, and accounting advisors before engaging in any transaction. Asset allocation and diversification do not guarantee a profit or protect against a loss. All references to potential future developments or outcomes are strictly the views and opinions of Richard W. Paul & Associates and in no way promise, guarantee, or seek to predict with any certainty what may or may not occur in various economies and investment markets. Past performance is not necessarily indicative of future performance.