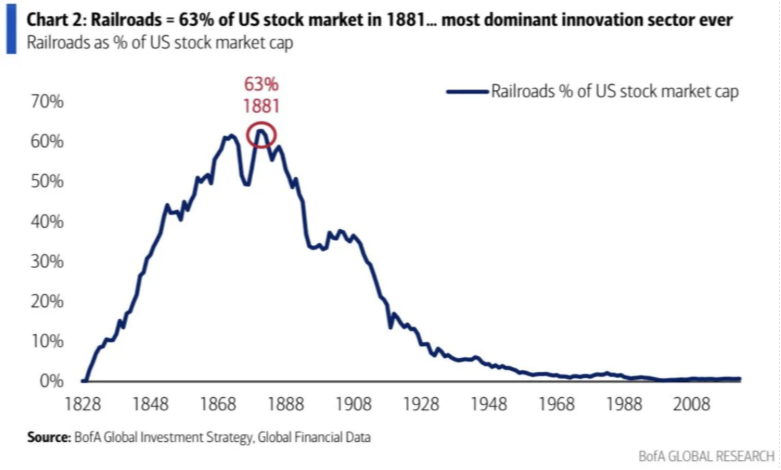

In the late 1800s, the railroad industry wasn't just transforming transportation; it was redefining the future. Steel tracks connected economies, shortened distances between cities, and unleashed waves of innovation. At the center of this transformation was J.P. Morgan, the financier who consolidated the railroads into powerful monopolies, reshaping the American industrial landscape. Investors rushed to buy stakes in giants like Pennsylvania Railroad, Union Pacific, and New York Central, fueling what became both a golden age, and eventually, a speculative frenzy in which railroad stocks accounted for 63% of the US stock market.

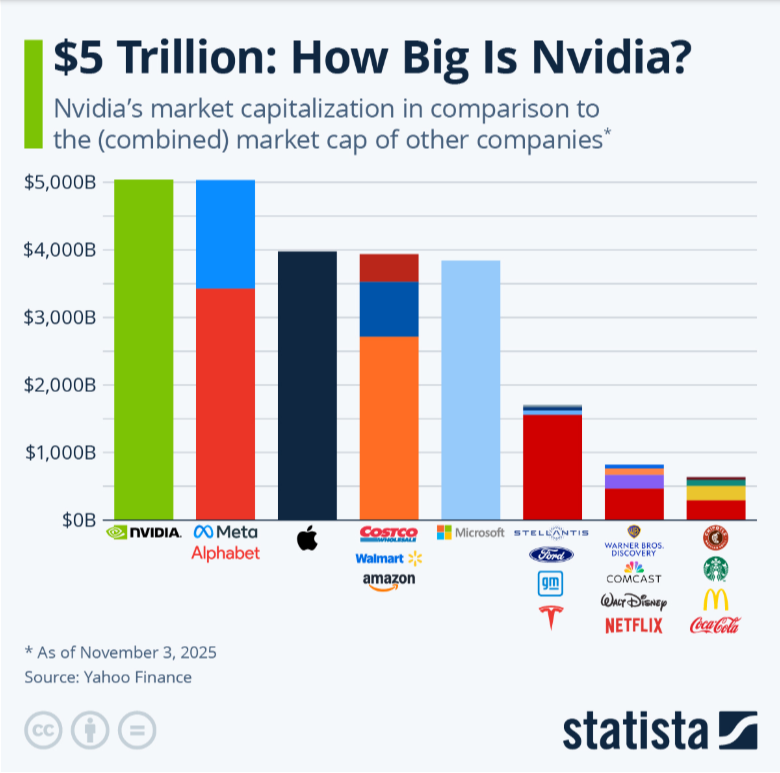

Fast forward to today, artificial intelligence is the new transcontinental railroad. And leading this relentless march is Nvidia (NVDA), the modern equivalent of Union Pacific. On October 29, 2025, Nvidia became the world’s first $5 trillion company.

Nvidia’s rise has been breathtaking. Since the release of ChatGPT in late 2022, Nvidia stock has soared over 12x, including a 50% jump this year alone. Its dominance in producing the GPUs that drive cutting-edge AI has made it the prime beneficiary of an unprecedented tech boom.

CEO Jensen Huang recently declared $500 billion in confirmed AI chip orders. The company is also building seven new supercomputers for the U.S. government—cementing its role as the backbone of the AI infrastructure.

The stock’s meteoric ascent has propelled Nvidia to a position of extraordinary influence:

- Over 8% of the S&P 500

- Nearly 10% of the Nasdaq-100

In financial history, few companies have commanded such a central role in global indices. Nvidia isn’t just a leader. It's a locomotive that pulls the entire market with it.

As the AI race accelerates, the web of relationships among its leading players has grown increasingly complex, sometimes dizzyingly so. Here’s a snapshot of just a few of the recent announcements:

- Nvidia + OpenAI: Nvidia and OpenAI announced a letter of intent to deploy at least 10 gigawatts of Nvidia systems for OpenAI’s nextgen AI infrastructure. As part of that agreement, Nvidia intends to invest up to $100 billion in OpenAI progressively as each gigawatt is deployed.

- AMD + OpenAI: AMD and OpenAI announced a multiyear partnership to deploy 6 gigawatts of AMD GPUs, beginning with a 1 GW deployment in the second half of 2026. As part of the deal, AMD has issued OpenAI a warrant for up to 160 million shares (~10% of AMD) contingent on milestones.

- Oracle + OpenAI + SoftBank (“Stargate”): OpenAI, Oracle Corporation and SoftBank Group announced five new U.S. AI datacenter sites, bringing the planned capacity of the Stargate LLC project to nearly 7 gigawatts, and the investment scope to over $400 billion over the next three years. The full target remains 10 gigawatts and $500 billion in investment for the project.

The chart below highlights this insane complexity even further:

These circular investments—part partnership, part competition, and part capital recycling—feel eerily familiar to the early days of American railroads. Giants like Pennsylvania Railroad and New York Central would invest heavily in rival lines to secure access to key regions, sometimes creating the illusion of unstoppable growth.

But here’s where the tracks diverge. Railroads, as you probably notice while waiting patiently for a train to pass, have a long, useful life. Compared to AI infrastructure that becomes obsolete at a staggering pace. The constant, expensive upgrades required for next-gen models could perpetuate a boom-bust cycle uniquely different from the slow decay of 19th-century steel.

In addition, the railroad boom was fueled largely by external capital and massive government land grants. Today's AI boom is being powered by the immense internal cash flows of tech giants like Microsoft, Google, Amazon, and Meta. These companies are funding the buildout from their own war chests. This fundamental difference in funding structure could change the dynamics of a potential bust, making it less about a sudden credit crunch and more about a strategic reassessment.

Let’s take a quick detour down memory lane. Back in 2021, a little company named Facebook rebranded itself as Meta and went "all-in" on the metaverse. Billions were burned. Bold promises were made. A virtual world of legless avatars was supposed to become the new reality. Then... it all hit a wall.

Could the same thing happen with AI?

Is AI a Bubble?

The answer isn't black or white.

Yes, certain stocks are clearly untethered from fundamentals. Companies with no revenue, no product, and no clear plan (except “we’re in AI!”) are seeing valuations soar.

No, because the leaders of this boom are spending tens of billions on infrastructure that already has real-world demand. Nvidia boasts a $500 billion backlog with a valuation that is not detached from reality, and the race for compute power among tech titans continues unabated.

Still, danger lurks in the market’s extreme concentration. The top 10 stocks now make up over 40% of the S&P 500, levels not seen in generations. This interconnectedness among the "Magnificent 7" creates a unique systemic risk.

And let’s be clear — this isn’t just about the Mag7. The entire AI stack is deeply interlocked. Apple is reportedly set to use a custom version of Google’s Gemini to power next-gen Siri — and that model runs on accelerator hardware co-developed by Google and NVIDIA. Those GPUs are born from a global semiconductor ecosystem: fabbed by TSMC, etched by ASML, designed with Cadence and Synopsys, tested or inspected by Teradyne and KLA. They end up in hyperscale data centers, mounted in Dell and HPE servers, cooled by Vertiv systems, and powered by utilities like NextEra and Dominion. Add in memory from Micron and Samsung, networking from Broadcom and Cisco, storage from Seagate and Western Digital, and the whole thing runs on cloud or bare-metal infrastructure from AWS, Azure, and others. It’s a tightly wound machine — where a snag in financing, silicon, energy, demand, logistics, or labor doesn’t just cause ripples. It could unleash a tsunami.

So, like any good advisor, we are constantly pondering the question: where could this go wrong? Here are some of the potential derailers:

- Progress stalls: If AI innovation slows, or becomes more iterative than breakthrough-driven, the market could cool quickly.

- Efficiency leaps: If large language models suddenly require far less compute (e.g. DeepSeek scare), the current GPU arms race could go the way of overbuilt rail lines.

- Hype fades: Big promises like OpenAI’s epic spending and partnership plans, could shrink, stall, or dissolve under pressure.

- Regulatory headwinds: Governments may step in with new rules on AI safety, data usage, or antitrust concerns, which could slow growth or complicate partnerships.

- Geopolitical friction: AI leadership is increasingly tied to national strategy. Export restrictions or trade conflicts could disrupt supply chains or access to talent.

- Execution risk: Even with billions on the table, these massive projects are hard to execute flawlessly—delays, integration challenges, or misaligned incentives could trip up progress.

That’s why the smart move isn’t to jump off the AI train, but to pick your seats carefully.

Focus on companies with:

- Real earnings

- Durable moats

- Tangible infrastructure

- Clear paths to long-term utility

And remember: today’s AI leaders dominate market indices. That’s concentration risk. For a retiree, diversification is as important as ever.

The AI revolution is real. But history reminds us: even in times of sweeping innovation, not every company—or investor—makes it to the last stop.

Disclosures

This material has been prepared for informational purposes only and should not be construed as a solicitation to effect, or attempt to effect, either transactions in securities or the rendering of personalized investment advice. This material is not intended to provide, and should not be relied on for tax, legal, investment, accounting, or other financial advice. You should consult your own tax, legal, financial, and accounting advisors before engaging in any transaction. Asset allocation and diversification do not guarantee a profit or protect against a loss. All references to potential future developments or outcomes are strictly the views and opinions of Richard W. Paul & Associates and in no way promise, guarantee, or seek to predict with any certainty what may or may not occur in various economies and investment markets. Past performance is not necessarily indicative of future performance.