The presidential election will be here before we know it, and the jockeying has already begun. Democrats and Republicans are using historical stock returns to justify why their candidate will be the best option for investors.

History only happens once, so it’s strange that both parties can use the same data to support two very different conclusions. Let’s do our analysis to see which party has done better.

There have been 24 election years since the S&P 500 began, and the index fell in four of them: 1932, 1940, 2000, and 20081. The Democratic candidate won in each except 2000, so the Republicans could argue that they have done better.

However, three of these years were during some of the worst economic downturns in our nation’s history. It’s unlikely that a Democratic win caused the Great Depression (1932), the dot-com bubble (2000), and/or the financial crisis (2008).

In fact, if an investor only used historical returns to decide whether to buy or sell during an election year, these data suggest buying irrespective of the winner. If only four years were down, then 20 years were either flat or positive. That’s 83% of the time. Not too shabby.

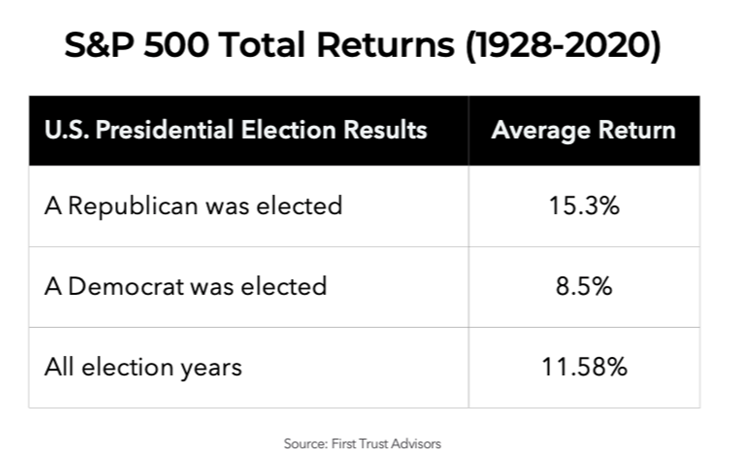

Since this analysis neither helps nor hurts either party, let’s dig deeper. The table below computes the average return in election years for both parties. Here, the Republicans appear to be the winner because the average return in the S&P 500 has doubled that of the Democrats. But the Left could argue that an election year is irrelevant. The election is in November, not January, so why judge the stock market on a candidate who hasn’t even been sworn into office yet?

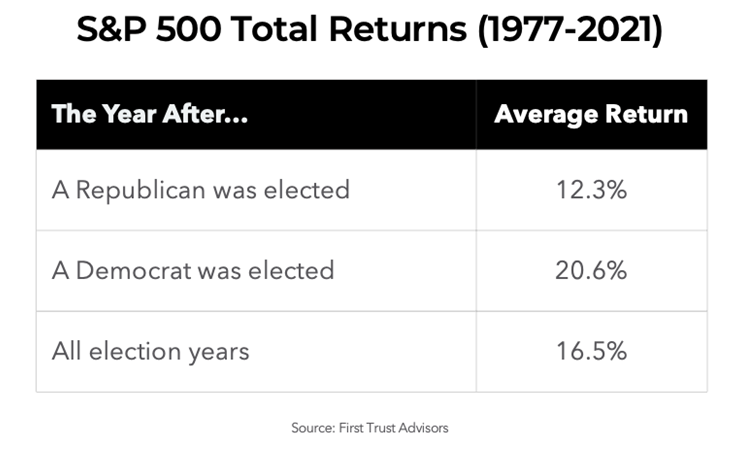

They could use the table below to counter. These are the average party returns of the S&P 500 during the first year of a presidential term (after being sworn in).

According to this table, the Democrats have clobbered the Republicans. But the Right could argue the date ranges for the two tables are different (the second one being a much shorter period). They could also claim that a rookie year for an administration means very little. Besides, the first year is just cleaning up the mess of the old administration, right?

The Democrats could then point out that the S&P 500 gained 14.9% during an average four-year Democratic presidential term and only 7.9% during a Republican one. Republicans could then argue that’s because there’s a lag effect in policy decisions. Hence, the fruits of their labor aren’t felt until after they leave office, and the mistakes of the Left don’t surface until they get back in the Oval Office.

Let’s stop here because this back-and-forth can go on forever. Historical stock returns can be sliced and diced a thousand ways until the results confirm whatever preconceived conclusion either party is trying to support.

Three types of lies

Investors succumb to dangers hidden within statistics because they carry powerful psychological triggers. It’s human nature to assume statistics are absolute, but too many self-interested pundits employ deceptive practices to drive agendas.

They put the cart before the horse by first deriving the conclusion that fits their narrative and then massaging the data under various lenses until they confirm what they want. It’s the exact opposite of a sound statistical analysis. The data should always drive the conclusion - not the other way around.

Data abuse is not relegated to just politics. It’s literally everywhere. Read How to Lie With Statistics by Darrell Huff to learn why every published statistic should be heavily scrutinized. This book was written in 1954, but the schemes unveiled remain prevalent today (it’s a quick read and involves very little math).

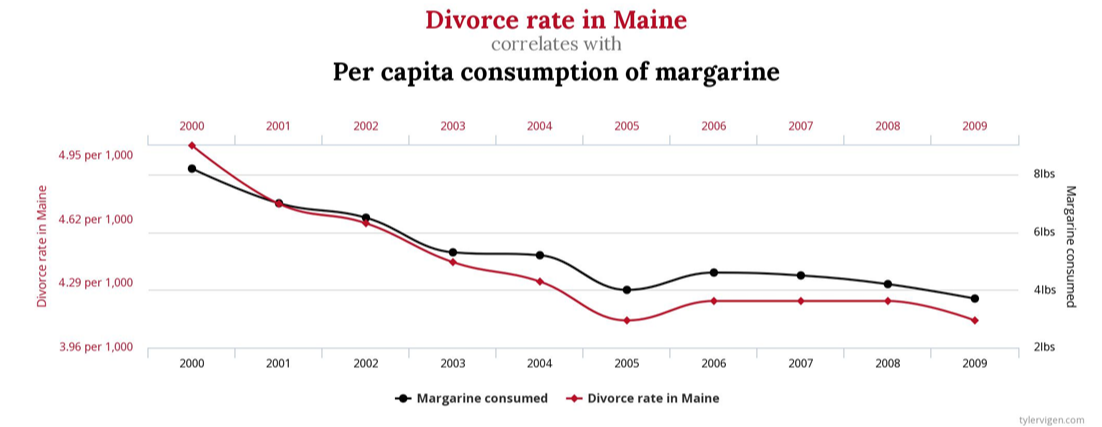

The chart below is another example of the dangers hidden within faulty statistical analysis. Upon first glance, this chart depicts an incredibly strong relationship between the divorce rate in Maine and the per capita consumption of margarine during the 2000s. However, this is more likely coincidental, and any relationship between the two is spurious.

Simply put, when it comes to statistics, consider them guilty until proven innocent.

“There are three types of lies – lies, damned lies, and statistics.”

- Benjamin Disraeli

The bottom line

If there is a reliable statistical relationship that says one political party is consistently better for stocks than another, I haven’t found it. I’d even wager it doesn’t exist for two reasons.

First, there haven’t been enough elections to build a large enough data set to derive a conclusion with a high degree of confidence. Second, it’s virtually impossible to imagine how any statistician could isolate the election from the several thousand other variables that drive stock prices and observe it in any meaningful way.

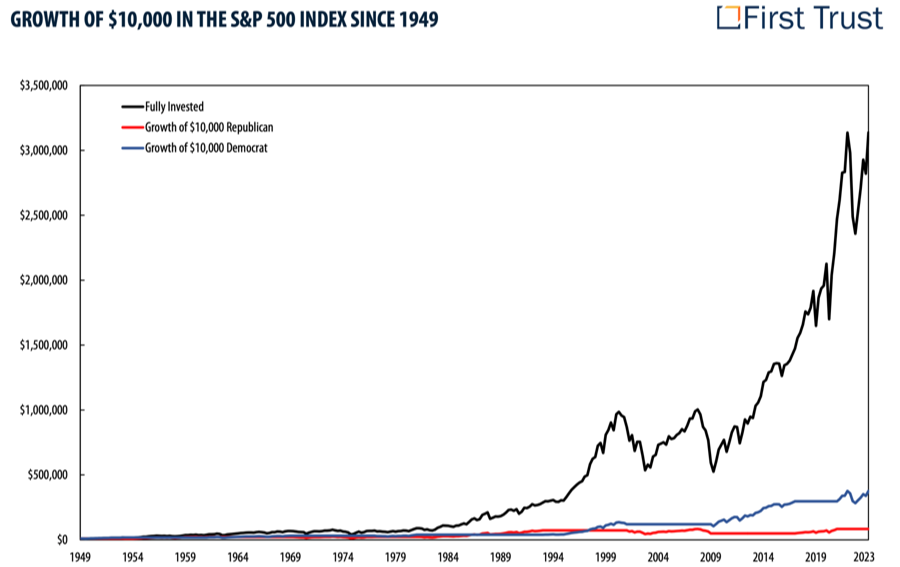

The chart below is all you need to know about the impact of presidential elections. The red line depicts owning stocks only when a Republican is president, the blue line a Democrat, and the black is staying fully invested. By far, the best investment strategy has been to own stocks irrespective of who’s sleeping in the White House. It’s not even close.

The bottom line is that no matter what either political party may preach, they are just one of many inputs into stock prices.

Sources

1 Bloomberg.

Disclosures