Two weeks ago, Trump Media (ticker: DJT) went public. As of April 9th, the company had a market value of $5 billion despite only earning $4.1 million in revenue and losing $58 million last year1. By any rational valuation metric, this stock is overpriced and likely one reason why DJT is the most popular stock to short right now2.

Short selling is one of the most controversial topics in investing. It’s also one of the most confusing, so let’s walk through the mechanics, the risks involved, and its role in markets.

Let’s assume that Stacy wants to “short” a fictitious company called Scam Corporation (fake ticker: SCAM) because she believes it’s a fraud. She logs into her online brokerage account and submits a trade to short 1,000 shares of SCAM at $50/share.

This is an order to sell stock she doesn’t own, so the broker facilitates this trade by looking in other client accounts for 1,000 shares of SCAM. The broker finds the shares in Mark’s account and then lends them to Stacy to sell. The proceeds of the sale (1,000 shares x $50/share = $50,000) are placed in Stacy’s account.

Mark is unaware that his shares were sold, but that’s ok. Brokers keep track of short positions to ensure Mark is not affected. For example, if he sold his shares seconds after Stacy borrowed them, the broker would find shares for Mark to sell.

Then one day, news breaks that Scam Corp is under investigation by the Justice Department and key executives have been arrested. The stock price falls to $5, and Stacy decides to “cover” her short position.

She places an order to buy 1,000 shares of SCAM at $5/share for a total of $5,000 (1,000 x $5/share = $5,000). The broker takes the shares purchased by Stacy and puts them back in Mark’s account to close out the trade. Stacy is left with a nice profit of $45,000 ($50,000 - $5,000 = $45,000).

To summarize, a short position is a loan. Stacy borrowed shares from Mark and then sold them for cash. After the share price fell, she used a portion of that cash to buy back the shares at a lower price and return them to Mark to close out her liability to him. Her profit is the leftover cash.

If it were that easy

While it may appear that Stacy just made some easy money, maintaining a short position is not for the faint of heart. There are three considerations worth discussing.

The first is the cost. Brokers charge a fee called the “borrow” to facilitate short sales. The borrow is based on supply and demand and changes daily. Heavily shorted stocks or those that trade infrequently can easily exceed 50% annually.

Existing short positions in Trump Media were paying annualized costs of 565% last week. Meaning, to break even on a new trade after one month, a short seller would have to see the share price of DJT drop by more than $30 from $48.81 at that time2.

Dividends are another cost. If SCAM paid $2/share in dividends, the broker would take $2,000 (1,000 shares x $2/share = $2,000) from Stacy’s account and place it into Mark’s account.

The second consideration is the direction of a stock’s asymmetric payout. Mark is “long” SCAM, so he can only lose what he put into the position (excluding transaction costs). He also has unlimited upside since a stock can theoretically rise forever.

The situation is reversed for short sellers. Stacy’s upside is capped at $50,000 because SCAM cannot fall below zero, but the downside is unlimited. For example, if SCAM surged from $50 to $350 in a week on news of a pending acquisition, she stands to lose six times her initial investment (in addition to the borrow paid to the broker and dividends paid to Mark).

This asymmetry can often fuel a “short squeeze.” This happens when a heavily shorted stock receives unexpected positive news. That’s not good for someone exposed to unlimited downside, and it can quickly ignite panic buying (the opposite of panic selling) as short sellers cover their positions. The ones who can’t get out first get squeezed as the stock soars higher.

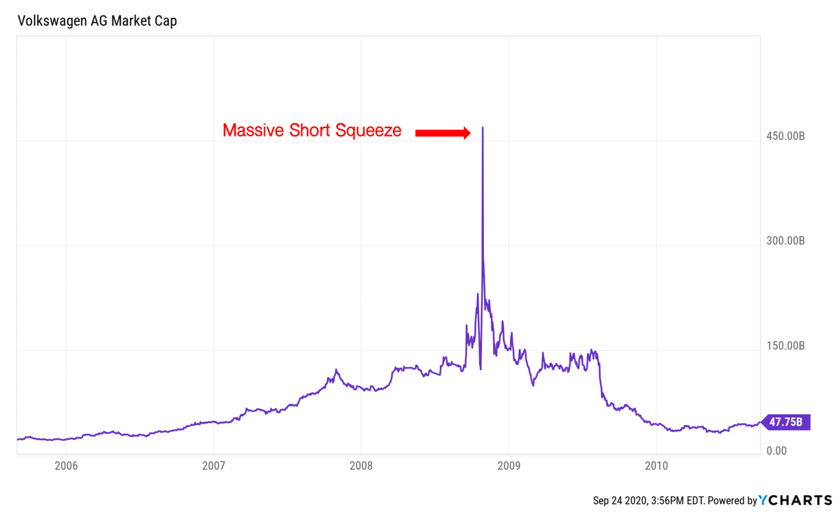

In 2008, Volkswagen’s short squeeze was so massive that it briefly propelled it to be the world’s most valuable company3. During the financial crisis, the company encountered challenges that inspired shorts to pile into the stock. Porsche then began buying a larger stake in Volkswagen, which caused shorts to cover their positions (buy back the stock). This created a vicious cycle, as seen in the chart below.

The third consideration is uncontrollable forces that have nothing to do with the investment thesis. For example, brokers have full authority to force short sellers out of their positions if a stock becomes too hard for them to manage. This can result in a loss for no reason other than operational challenges at the brokerage.

Margin requirements can also cause problems. Since short positions have unlimited downside potential, brokers require short sellers to keep account levels above thresholds. Meaning, if Stacy’s short in SCAM is working, but the rest of her portfolio is losing money, her broker may close out her short position because the account value falls below the required level.

There have also been instances where the short thesis is correct, but the fraudsters received protection from regulators. One of the largest scandals collapsed in June 2020, when Wirecard’s auditors refused to sign off on their books. For over a decade, there had been accusations of fraud from prominent short sellers across the globe. However, German authorities refused to take these seriously4.

The bottom line

It’s hard to think of a group of investors that is despised more than short sellers. They are demonized by the press, sued by their targets, and even vilified by regulators. But this cohort serves an invaluable purpose for a well-functioning market. They are the watchdogs that sniff out bad things that can hurt investors. They also serve as a reminder to management that someone is analyzing their every move.

Think about it this way. Try to name a single major fraud unearthed by regulators over the last two decades. I can’t. Short sellers and journalists expose the big ones. However, journalists tend to rely on intel from whistleblowers and other sources. The real skill lies with professional short sellers. They are capable of digesting mountains of financial data and connecting the dots.

Furthermore, show me a market that cannot be shorted, and I’ll show you one poised for trouble. The housing market ran wild before 2008 because there was no way to express a negative view. WeWork lit billions on fire for years, leading to its failed IPO in 2019. Maybe they would have been wiser if the market for venture capital offered a way for short sellers to keep it in check.

However, not all short sellers are saints, and the opportunity for profit is often so powerful that it can coerce some to publish phony data and blatant lies. Short sellers aren’t always successful, either. Prominent hedge funds have led countless short campaigns with deep pockets that died on the vine simply because they were unable to sway other large money managers.

The bottom line is that short sellers are integral to markets but leave it to the professionals. The requisite skill and ability to manage risk are traits that are often too hard to acquire on your own.

Sources

1 Bloomberg. As of 4/3/2024

2 https://www.cnbc.com/2024/04/03/trump-media-is-the-most-expensive-us-stock-to-short-by-far.html

3 https://www.warriortrading.com/volkswagen-short-squeeze/

Disclosures

This material has been prepared for informational purposes only and should not be construed as a solicitation to effect, or attempt to effect, either transactions in securities or the rendering of personalized investment advice. This material is not intended to provide, and should not be relied on for tax, legal, investment, accounting, or other financial advice. You should consult your own tax, legal, financial, and accounting advisors before engaging in any transaction. Asset allocation and diversification do not guarantee a profit or protect against a loss. All references to potential future developments or outcomes are strictly the views and opinions of Richard W. Paul & Associates and in no way promise, guarantee, or seek to predict with any certainty what may or may not occur in various economies and investment markets. Past performance is not necessarily indicative of future performance.