Most Medicare beneficiaries pay a standard premium for Part B coverage, but higher income retirees face an additional surcharge called IRMAA that can significantly increase their monthly costs. For 2026, the standard Part B premium is $202.90 per month, but depending on your 2024 income, you could pay anywhere from $284.10 to $689.90 monthly.

What is IRMAA?

IRMAA stands for Income Related Monthly Adjustment Amount. This surcharge applies to both Medicare Part B (medical insurance) and Part D (prescription drug coverage) for beneficiaries whose modified adjusted gross income exceeds certain thresholds. According to Centers for Medicare & Medicaid Services (CMS), approximately 8% of people with Medicare Part B pay these income related monthly adjustment amounts, with a similar percentage affected in Part D.

The Social Security Administration determines your IRMAA based on tax return information it receives from the IRS. If you owe IRMAA, Social Security will send you a notice explaining the determination and your monthly premium amount. For Part B, the IRMAA is built into your total premium amount, while for Part D, the IRMAA surcharge is added on top of your plan's regular premium.

How your income is calculated

The income figure that matters for IRMAA is your modified adjusted gross income, or MAGI. For Medicare purposes, MAGI equals your adjusted gross income from your tax return plus any tax-exempt interest income. This means municipal bond interest counts toward IRMAA even though it doesn't create federal income tax.

Social Security uses a two-year lookback when determining IRMAA. For 2026 Medicare premiums, they examine your 2024 tax return that you filed in 2025. Social Security relies on the most recent return the IRS provides to them, which is typically from two years prior. If you filed married filing jointly, they look at your combined MAGI, while separate filers have different thresholds.

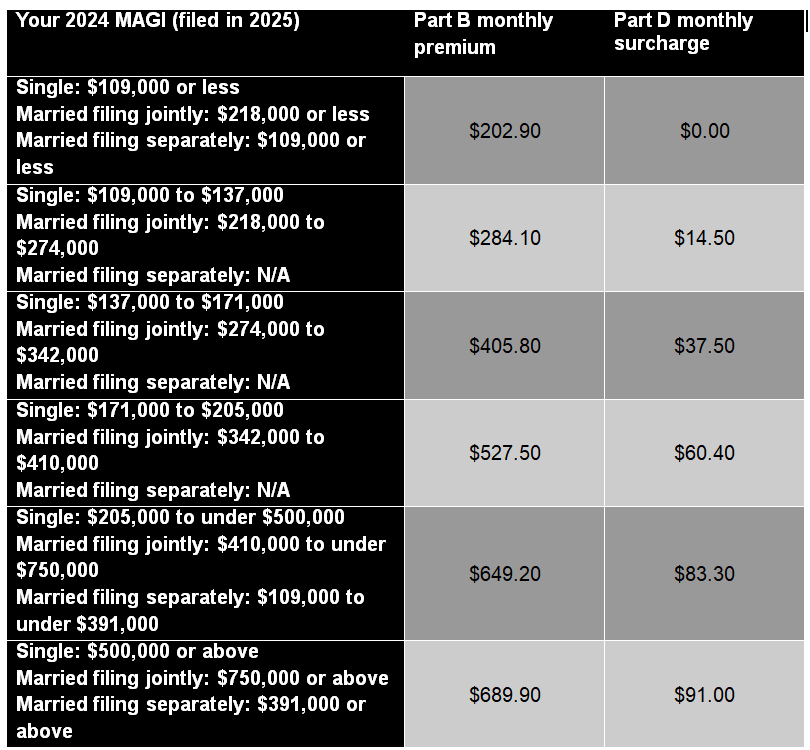

2026 income brackets and premium amounts

The IRMAA structure uses five income tiers above the base premium level. The brackets below show 2024 MAGI ranges (the income year that determines your 2026 premiums) and the corresponding monthly costs.

Part B & D Monthly Premiums for 2026

Source: https://www.cms.gov/newsroom/fact-sheets/2026-medicare-parts-b-premiums-deductibles

Source: https://www.cms.gov/newsroom/fact-sheets/2026-medicare-parts-b-premiums-deductibles

The cliff effect at bracket edges

One important feature of IRMAA is that each bracket applies to your entire premium, not just the income above the threshold. If a single filer has $136,999 in MAGI, they pay $284.10 monthly for Part B. If that same person has $137,001 in MAGI, crossing into the next bracket by just $2, their monthly premium jumps to $405.80. Over twelve months, that extra $2 of income costs $1,456.40 in additional Medicare premiums.

This cliff structure makes year-end tax planning especially valuable for people near bracket edges. Strategies like timing capital gains, managing IRA distributions, or adjusting Roth conversion amounts can keep income below the next threshold.

Appealing IRMAA based on life-changing events

The two-year lookback can create situations where your current income no longer reflects what you earned two years ago. Social Security recognizes this and allows you to request a new determination if you experienced certain life-changing events that reduced your income.

The qualifying events include marriage, divorce or annulment, death of a spouse, work stoppage, work reduction, loss of income producing property, loss of pension income, and receipt of a settlement payment from an employer or former employer because of closure or bankruptcy. Social Security specifies that you must have experienced one of these events and your income must have declined because of it.

To request a new determination, you must complete form SSA-44, which is the Medicare Income-Related Monthly Adjustment Amount Life-Changing Event form (download here). You'll need to provide information about the life changing event, estimate your current year income, and potentially provide supporting documentation. Social Security states that if you are requesting a new decision because a life changing event reduced your income, you generally do not need to file a formal appeal of the original IRMAA decision.

The SSA-44 form is not for general appeals about the accuracy of your income information. If Social Security used the wrong tax year or didn't account for an amended return, you should contact them to provide the correct tax return information rather than filing an SSA-44. Social Security explicitly states that if they used an older tax return and a more recent return is now available, or if you filed an amended return that changed your MAGI, you should contact them with documentation of the updated tax information. For further info on the appeals process, follow this link.

Temporary Surcharge, Not a Permanent Tax

The standard Medicare Part B premium sits at $202.90 per month for 2026. For a married couple both enrolled in Medicare, a 40% surcharge amounts to roughly $1,948 in extra costs over the course of the year. Households with over $218,000 in income already face significant tax obligations, and paying an additional ~$2,000 can be frustrating even if it represents less than 1% of total income. The cliff nature of the brackets is what often causes the most irritation, as earning just a few dollars over the threshold triggers the full surcharge for the entire year.

If your income from two years prior was elevated and you do not qualify for a life changing event appeal, you simply pay the higher premiums for that specific year. These additional funds go directly into the Medicare trust fund to support the program's solvency for all beneficiaries.

The good news involves the annual reset of these calculations. Social Security re-evaluates your income every year. If your high income resulted from a one-time occurrence, like selling a property or recognizing large capital gains, your premiums will automatically drop back down once your income record reflects a more typical year. Keep in mind, paying the surcharge for a single year is an annoying but temporary expense rather than a permanent increase in your fixed costs.

Disclosures

This material has been prepared for informational purposes only and should not be construed as a solicitation to effect, or attempt to effect, either transactions in securities or the rendering of personalized investment advice. This material is not intended to provide, and should not be relied on for tax, legal, investment, accounting, or other financial advice. You should consult your own tax, legal, financial, and accounting advisors before engaging in any transaction. Asset allocation and diversification do not guarantee a profit or protect against a loss. All references to potential future developments or outcomes are strictly the views and opinions of Richard W. Paul & Associates and in no way promise, guarantee, or seek to predict with any certainty what may or may not occur in various economies and investment markets. Past performance is not necessarily indicative of future performance.